How Uganda’s Agriculture Insurance Scheme Reached 1 Million Farmers

Uganda's Agriculture Insurance Scheme protects 1M smallholder farmers from climate risks. Learn how it works, what it costs, and how to be part of it today.

Climate change has turned farming into a gamble for millions of Ugandan smallholder farmers. When rains fail or refuse to stop, an entire season’s livelihood can disappear overnight. Yet a powerful solution has been quietly operating since 2016.

We sat down with Attra Atukunda, the Business Development and Partnerships Lead at the Agro Consortium (AIC), to explain how the Uganda Agriculture Insurance Scheme works, what it costs to access insurance, and why every Ugandan farmer deserves to know it exists.

Qn: What is the Uganda Agriculture Insurance Scheme, and how did it come about?

Born in 2016 out of a need to protect farmers from an increasingly erratic climate, the scheme is a public-private partnership (PPP) between the Government of Uganda, represented by the Ministry of Finance and a consortium of 14 private insurers, with AIC as the mandated implementing body.

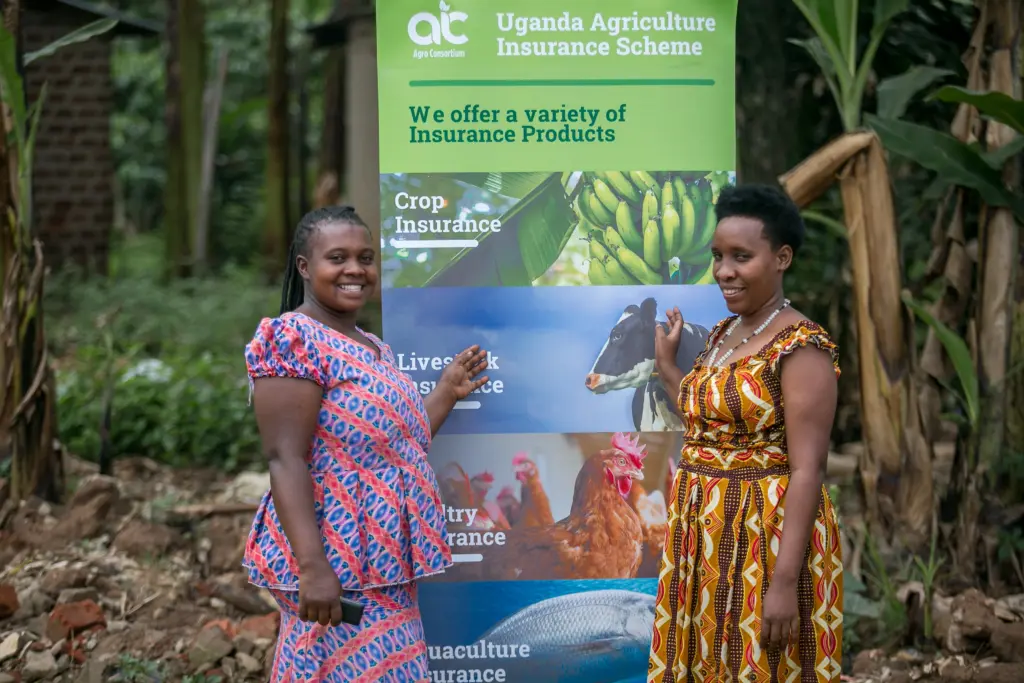

Because it is a national scheme, it covers crops, livestock, and aquaculture across the entire country from maize growers in Eastern Uganda to coffee farmers in the West and fish farmers along Lake Victoria. No value chain is excluded.

The scheme also has a strong gender dimension. AIC has been intentional about growing women’s participation, and today 30% of the one million insured farmers are women, achieved through targeted outreach to women farmer groups and gender-sensitive product design. This inclusion is not incidental; it is a core part of AIC’s mandate.

| Worth noting:95% of all insured farmers are smallholder farmers with five acres or less. This is not a scheme designed for only large commercial operations, it is built specifically for the ordinary Ugandan farmer who needs protection most. |

Qn: How does the government subsidy work, and who qualifies?

The government contributes an annual premium subsidy of UGX 5 billion to keep costs genuinely affordable for farmers. This subsidy is applied automatically at the point of calculation, farmers simply pay their portion, and the government’s contribution is already factored in. There is no separate application or bureaucratic process to navigate.

The subsidy is divided into three tiers based on farm size and location:

| Category | Definition | Farmer Pays | Govt. Covers |

| Smallholder (≤5 acres) | Small farms, 5 acres or below | 50% | 50% |

| Large-Scale (>5 acres) | Farms above 5 acres | 70% | 30% |

| High-Risk Areas | Historically vulnerable regions | 20% | 80% |

Farmers in high-risk areas, regions historically affected by climate related disasters including severe drought or persistent flooding receive an 80% government subsidy regardless of farm size. This is the highest tier of support, deliberately targeted at communities most exposed to climate shocks.

It is also worth noting that these premium rates are not fixed,they vary by region, enterprise and the specific product chosen. AIC continuously refines its products to match the changing needs of farmers.

As Attra noted, “we have grown, we have continuously refined and reworked our solutions to speak to the ever- changing needs of the farmer.”

HOW IT ACTUALLY WORKS

Qn: I am a maize farmer with one acre. What does insuring my crop look like in practice?

AIC needs the following things from you:

- your acreage,

- your expected yield per acre,

- your selling price per kilogram.

- Location- district/ subcounty

These are used to determine your insured value and the and premium payable

Here is a practical example using maize, one of the most commonly insured crops in Uganda:

| EXAMPLE — MAIZE FARMER, 1 ACRE | |

| Yield per acre (average) | 800 kg |

| Selling price per kg (average) | UGX 800 |

| Total insured value (1 × 800 × 800) | UGX 640,000 |

| Premium at 5.5% index rate | UGX 35,200 |

| After 50% government subsidy | Farmer pays: UGX 17,600 |

For just UGX 17,600, a smallholder maize farmer protects a harvest worth UGX 640,000. For two acres, both the insured value and the premium double, but the affordability principle holds.

Rates vary by region and crop, but the design is consistent: affordable by intent, not by accident.

Beyond maize, AIC insures a wide range of value chains. Coffee farmers, poultry farmers, aquaculture operators, and input-dependent producers of all kinds are covered. If you farm it in Uganda, there is very likely an insurance product tailored to protect it.

Qn : What changed from the old insurance model, and why does that matter for farmers today?

When the scheme launched in 2016, AIC used Traditional Multi-Peril insurance, a model that required a physical assessor to visit the farm at every stage of crop growth, from planting through to harvest. Each visit added cost, and those costs were ultimately passed on to farmers through high premiums, making the product unaffordable for smallholders.

AIC therefore shifted to index insurance powered by satellite monitoring technology. Satellites track weather and crop conditions in real time across the country. If a drought develops or excessive rainfall is recorded, the data triggers claims automatically, without the farmer needing to report or wait for a ground visit.

This is not a theoretical benefit. Attra confirmed that farmers regularly receive payouts before they have even thought to call, because the satellite data has already identified and flagged their loss. This shift from reactive to proactive claims processing is what makes index insurance genuinely different and genuinely trustworthy.

| The result: Moving from expensive on-farm assessments to satellite-driven index insurance reduced premiums significantly and explains how AIC grew from just 20,000 insured farmers in 2016 to over one million today. |

Qn: When disaster strikes, what does the payout look like ?

In the event of a total qualifying loss drought, excessive rainfall, pests, or another covered peril the farmer receives 70% of the total insured value. The remaining 30% is the farmer’s own excess: their contribution toward the loss. Using the maize example, a total loss on a UGX 640,000 harvest results in a payout of UGX 448,000.

The 30% excess is not punitive, it is structural. It exists to prevent insurance fraud (a documented reality even in agriculture), and to ensure that farmers remain invested in their crops throughout the season. As Attra put it directly: “If you have insured your garden, it does not mean you don’t weed. You need to do exactly what you would do whether there was insurance or not.”

The goal of insurance is indemnity, restoring the farmer to the position they were in before the loss, not generating profit from a disaster. The 70% payout accomplishes exactly this: it covers the loss while keeping the farmer accountable for their own role in the outcome.

Note; These deductibles vary based on districts and insurance product

| The principle: Insurance is a safety net, not a replacement for good farming. The 70% coverage is designed to restore the farmer’s financial position after a genuine climate event, while preserving every incentive to produce. |

“95% of our one million insured farmers are smallholder farmers, the underserved market that actually sees and understands the need.”

— Attra Atukunda Business Development and Partnerships Lead AIC Uganda-

HOW TO ACCESS IT

Qn: How does a farmer actually get insured? Do they walk into an office alone?

AIC works primarily through an ecosystem model, partnering with aggregator organisations that already have established farmer relationships. Because individual policies can be costly to administer at small scale, farmers are strongly encouraged to insure collectively through cooperatives or farmer groups, which most Ugandan farmers are already attached to in some form.

These aggregators span several categories, each with its own business reason for wanting insurance in the mix:

| OFF-TAKERS: Protect supply chains when drought prevents farmers from delivering contracted produce. | INPUT DEALERS: Protect credit advanced to farmers if the season fails, repayment is still secured. |

| BANKS, MFIS & SACCOS: Protect agriculture loan portfolios from climate-driven defaults, enabling more and bolder lending. | COOPERATIVES & GROUPS: Aggregate members for collective, affordable insurance with simplified administration. |

For farmers not yet connected to a cooperative,

AIC has regional offices in Gulu, Fort Portal, Mbale, Jinja, and Kampala. Each office is staffed by agronomists who go on the ground to conduct training and farmer engagement.

Farmers can also call the toll-free helpline: 0800 300 021, where multilingual teams are ready to assist in local languages at no cost to the caller.

AIC has also insured agriculture production loans worth over UGX 3 trillion ($798M) since 2016 as a direct result of lenders gaining confidence to extend more credit to farmers once insurance is in the picture.

This means the scheme does not just protect farmers from losses; it actively unlocks access to financing that was previously out of reach.

Qn : Can you tell us more about the training AIC provides?

Training is one of AIC’s core mandates and it begins before a single contract is signed. The philosophy is clear: a farmer must genuinely understand the product before committing to it. AIC deploys field teams directly to cooperatives and farmer groups to run these sessions.

Critically, the training is hybrid: it covers both insurance literacy and practical agronomic best practices. This means farmers are better equipped not only to understand their policy, but to improve their farming, reducing the likelihood of a loss in the first place.

AIC also operates a multilingual call centre accessible toll-free that remains available throughout the season. As Ms. Attra emphasised, “it is important that the customer journey does not end” at the point of premium payment.

Ongoing support, follow-up visits, and open lines of communication are all part of how AIC maintains trust with farming communities over the long term.

OVERCOMING SKEPTICISM

Qn: Many Ugandan farmers are skeptical of insurance. How has AIC addressed that?

“The biggest challenge is trust,” Ms. Attra l acknowledged plainly, “and rightfully so.” Insurance asks people to pay for something they hope never to use. For farmers who have historically been let down by financial services not designed for them, that skepticism is rational and AIC takes it seriously.

The most powerful response has been the evidence itself. Since 2016, AIC has paid out over UGX 54 billion ($14.3M) in verified claims to farmers across Uganda, across different crops and different regions. These are not projections, they are recorded, auditable payouts. After every payout cycle, AIC returns to the ground to collect video and written testimonials from farmers who received compensation, then shares them on social media so that peers can convince peers in ways no corporate campaign ever could.

Importantly, Uganda’s insurance sector is regulated by the Insurance Regulatory Authority (IRA). Any farmer who is unhappy with how a claim is handled has a formal and accessible escalation path. This layer of regulatory oversight was not always available to Ugandan farmers and represents a meaningful assurance that the system has accountability built into it.

The growth trajectory tells its own story. AIC started with approximately 20,000 insured farmers in 2016. Today that number exceeds one million farmers, 95% of them smallholders who chose to participate. That scale of voluntary uptake, among the most skeptical segment of any financial market, is the clearest possible proof that the product delivers on its promise.

Qn: Who else can partner with AIC, beyond individual farmers?

AIC describes itself as “the risk partner for the entire agriculture ecosystem”. It reflects a deliberate and practical operating model, every actor along Uganda’s agricultural value chain has a clear reason to engage with AIC, because risk is embedded across the system, not just at the farm level.

Attra identified a number of distinct partnership categories in addition to farmer cooperatives, each with its own rationale:

| AGTECHS & FINTECHSAdd insurance as a meaningful value-add to farmer-facing platforms, deepening engagement, and retention. | DEVELOPMENT PARTNERS & NGOSIntegrate AIC’s training and insurance into climate resilience or food security programmes for sustainability and lasting impact. |

| OFFTAKERS & INPUT COMPANIESBundle insurance with products to de-risk receivables and give farmers greater confidence to invest. | FINANCIAL INSTITUTIONS, MFIs & SACCOSEmbedding agriculture insurance to protect portfolios and unlock more credit to farmers. |

The partnership model is deliberately flexible, designed to fit the structure, reach, and mandate of each partner rather than requiring everyone to conform to a single template. As Attra noted, AIC understands that “models are very different” across organisations, and that the best outcomes come from building solutions that speak to each partner’s specific need.

For any organisation interested in exploring a partnership, AIC is actively open to new conversations. The starting point is a conversation and that conversation can begin by calling the toll-free number;- 0800300021 , sending an email on info@aic.ug, or visiting any of the five regional offices across Uganda.

Disclaimer

Africa Agribusiness News (AAN) is committed to informing and empowering agricultural communities across Africa with timely and relevant industry information as per our mandate. This article has been compiled from materials provided by the Agriculture Insurance Company of Uganda (AIC) and is intended for informational purposes only. Readers are advised to verify all details directly with AIC before making any insurance or financial decisions.

No Comment! Be the first one.